GDP base revision may push FY26 growth higher; history points to upward bias

Read Time:2 Minute, 42 Second

Shift to 2022-23 base year could lift headline growth and nominal GDP estimates as improved data coverage feeds into calculations

- India’s FY26 GDP growth may rise after new base year revision

- Past base year changes have typically boosted reported growth

- Revised data could push India closer to $5-trillion economy goal

India’s economic growth for FY26 could see an upward revision once the government releases GDP data under the new 2022-23 base year later this week, with past revisions indicating that such statistical recalibrations typically nudge headline growth higher.

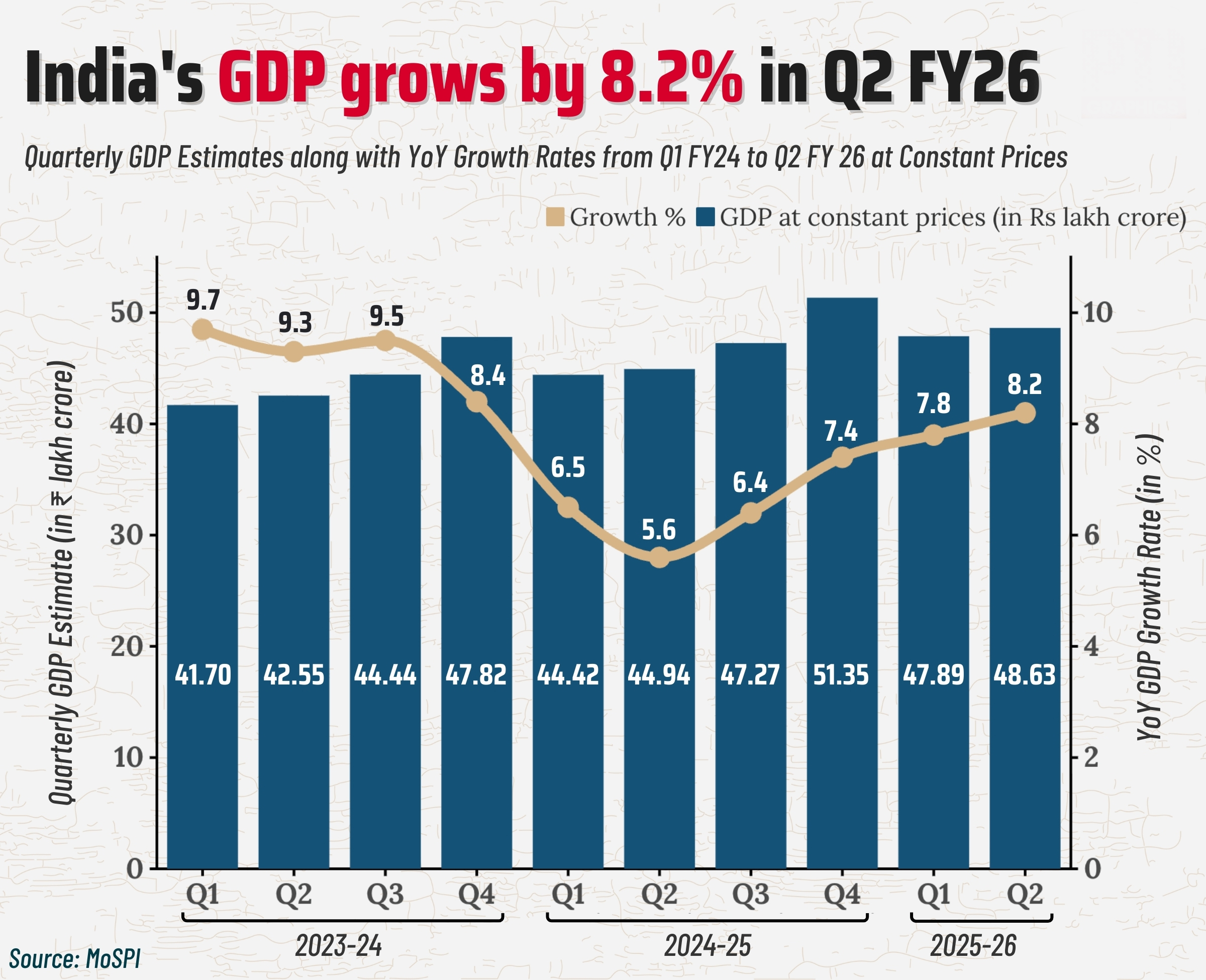

Advance estimates released on January 7 had pegged FY26 growth at 7.4 percent, but those numbers were calculated using the older 2011-12 base year. Fresh estimates due on February 27 are expected to incorporate updated methodologies, broader datasets and revised sectoral weights, potentially altering the growth trajectory.

Historical experience suggests base-year revisions often result in stronger reported growth, particularly when statistical coverage expands. If earlier patterns hold, FY26 growth could see an upward adjustment of around 0.25 percentage points or more.

Growth usually sees upward revisions with new series

1993-94 | 1999-2000 | |

|---|---|---|

| FY01 | 4.4 | 4.4 |

| FY02 | 5.8 | 5.8 |

| FY03 | 4.0 | 3.8 |

| FY04 | 8.5 | 8.5 |

| FY05 | 6.9 | 7.5 |

| 1999-2000 | 2004-05 | |

| FY06 | 9.5 | 9.5 |

| FY07 | 9.7 | 9.7 |

| FY08 | 9.0 | 9.2 |

| FY09 | 6.7 | 6.7 |

| 2004-05 | 2011-12 | |

| FY13 | 4.7 | 5.1 |

| FY14 | 5.0 | 6.9 |

The last major revision, when the base year shifted to 2011-12 from 2004-05, significantly reshaped growth estimates. FY13 growth was revised upward by roughly 0.35 percentage points, while FY14 saw a much larger revision of nearly 1.9 percentage points, lifting growth to 6.9 percent. That revision also incorporated the Ministry of Corporate Affairs database, substantially expanding the universe of firms captured in GDP calculations.

Earlier revisions were more modest. The move to the 2004-05 base from 1999-2000 raised growth by only about 0.04 percentage point on average, while revisions from the 1993-94 base produced marginal changes of around 0.06 percentage point.

Nominal GDP has historically shown larger adjustments than real growth. Across four revision cycles since the early 1980s, nominal growth has typically seen an upward revision of roughly half a percentage point, reflecting improved measurement of prices, services output and corporate activity. For instance, nominal growth in FY13 was revised from 12.2 percent to 13.1 percent, while FY14 was lifted from 12.3 percent to 13.6 percent after the 2011-12 base revision.

The upcoming shift to the 2022-23 base is expected to better capture newer sectors, including the digital economy, alongside updated consumption patterns and improved data sources. These changes could influence both real and nominal GDP estimates.

If historical trends repeat, FY26 real growth could edge closer to 7.6 percent or higher. Such revisions would have implications beyond headline growth, affecting fiscal ratios, debt metrics and macroeconomic projections linked to GDP size.

Nominal GDP adjustments could also move India closer to the $5-trillion economy milestone. Past revisions suggest nominal GDP levels tend to rise by about 1.7 percent on average following base updates. Budget estimates had already projected the economy to reach around Rs 393 lakh crore in FY27, a figure that could cross Rs 400 lakh crore once revised GDP data are incorporated.

Happy

0 %

Sad

0 %

Excited

0 %

Sleepy

0 %

Angry

0 %

Surprise

0 %

Average Rating